Personal Finance

Americans relying less on cash, more on credit cards may pay more fees. Here’s why.

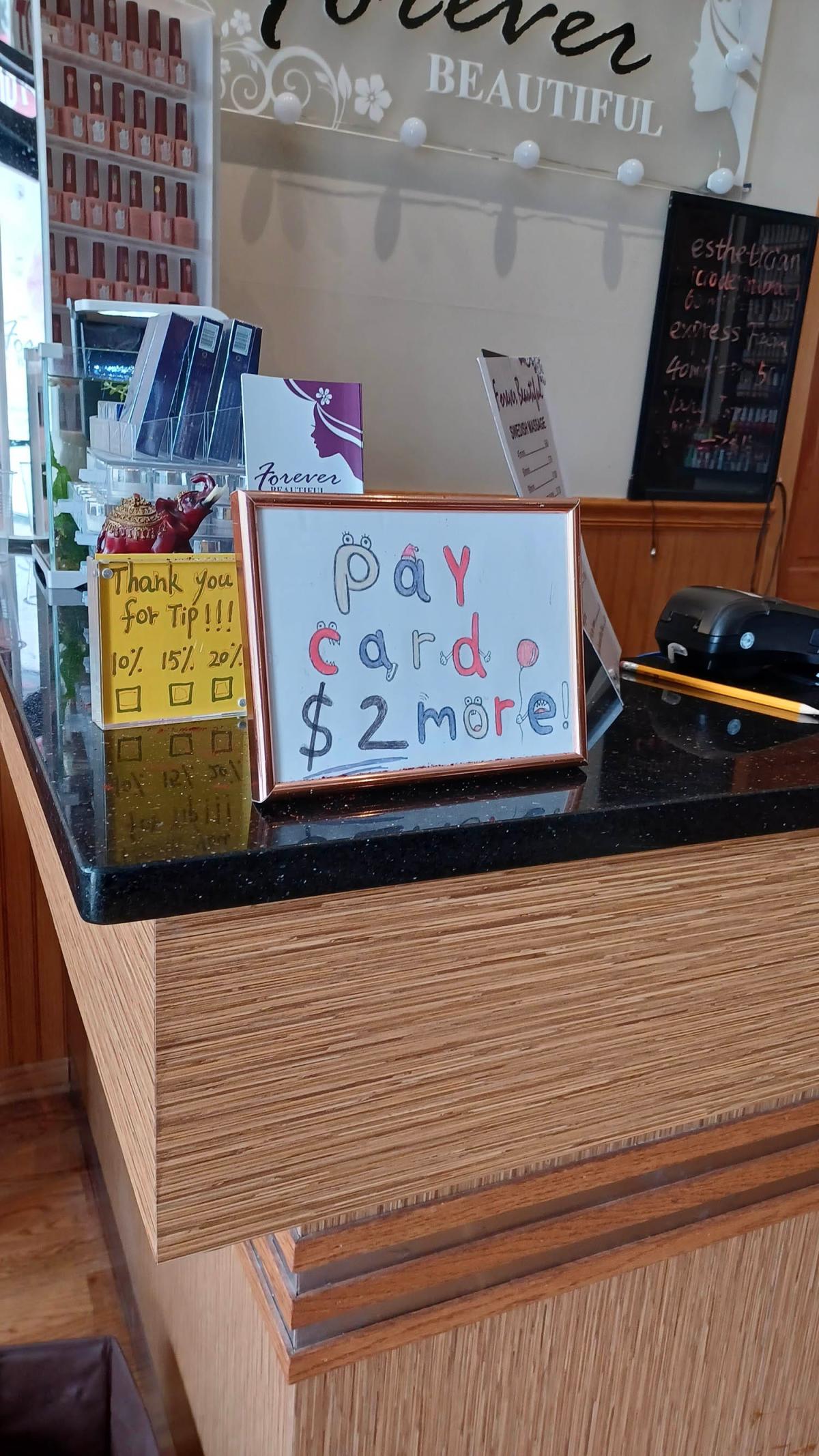

When Brian Marks bought a pastry last summer at a bakery he had been frequenting for years, he noticed an extra charge on his receipt. Turns out, it was a new fee for using his credit card.

Since then, he’s spotted the fee popping up at more and more businesses.

“Sometimes it’s characterized as a service fee instead of a credit card fee,” said Marks, executive director of the Entrepreneurship and Innovation Program at the University of New Haven in Connecticut. “In some instances, businesses aren’t even posting it… More and more so, these fees are borne by the consumer (rather) than seller.”

What is a credit card fee?

Whenever you use your credit card to make a purchase, the store must pay a behind-the-scenes interchange fee to process that payment. Most of that fee goes to the bank issuing the card, but companies like Visa and Mastercard also receive a smaller fee for processing the payment through their networks.

Fees are charged as a percentage of the total sales amount in each transaction, but the percentage charged to each merchant, whether at a physical store or online, varies. On average fees run about 2%.

Factors that determine what percentage the merchant is charged include: type of merchant (department store, convenience store, gas station); type of payment technology used by the merchant; whether the purchase is online or in person; and the type of card.

Businesses used to swallow the costs of credit card processing, figuring that accepting credit cards would bring in more business to offset the costs. However, after more than two years of scorching inflation that’s boosted the price of everything, businesses – especially smaller ones — sought ways to offload some costs to survive. Credit card fees were an obvious choice for many.

How are credit card fees passed on to consumers?

Businesses usually pass on the cost of credit card processing by:

-

Charging customers an additional amount if they pay by card. In general, the charges are a percentage of the total purchase, typically the 1.5% to 3.5% that credit card companies charge merchants to accept and process the transaction. Sometimes, though, they’re flat fees. It’s important to note these fees can be called different names: surcharge, service fee, or convenience fee. Both for-profit and nonprofit companies can charge the fees.

The American Cancer Society, for example, asks donors to pay a 5.5% fee to help pay “transaction & processing fees, web support and receipts. It also includes costs associated with cyber security, fraud, and customer service etc.,” it said.

Utility company Consumers Energy said that starting this month, autopay customers must have payments directly withdrawn from bank accounts instead of charged to debit or credit cards. People who pay by debit or credit card would be charged $2.99 per transaction. “Like many companies, we are encouraging customers to use payment methods that don’t incur fees that could increase costs in the future,” said Brian Wheeler, Consumer Energy media relations manager. “More than two-thirds of all energy providers take this approach, as do businesses of all types.”

-

Offering a discount if customers pay cash. Discounts also are a percentage of your bill or a flat amount. For example, T-Mobile changed its $5 per line autopay discounts earlier this year to only apply to customers who pay by debit card or linked bank account.

Why are we seeing more credit card fees?

Businesses, burned by rising costs, are looking for ways to cut expenses.

“The cost of credit card fees is our number three cost of doing business behind payroll and rent,” Patti Riordan, owner of Smoke Stack Hobby Shop in Lancaster, Ohio, said.

Merchants paid $126.4 billion last year in processing fees to accept credit card payments, up 20% from 2021, according to global payments researcher Nilson Report.

The Electronic Payments Coalition (EPC), an advocate for credit unions, community banks, and payment card networks, attributes the jump to Americans preferring to use credit cards.

The reasons range from fraud prevention and the safety of not carrying cash to reward points and cashback that encourage spending, it said.

In the three months through June, credit card balances soared to a record high of $1.03 trillion, the New York Federal Reserve said.

Is it legal for businesses to charge a credit card fee?

A credit card surcharge isn’t legal in every state, but a discount is.

Surcharges are illegal in Connecticut, Maine, Massachusetts, and Oklahoma, according to card processor Visa, as of April 15.

Why don’t businesses raise prices to cover this cost?

Businesses have already increased prices significantly in the past few years as inflation surged, and some are hesitant to raise them further.

Restaurants “don’t do that because menu prices tend to be sticky,” said Marks. “So, they find ways to segregate it.”

Since owners want to avoid changing prices too often — moves that can startle customers and cost time and money to publicize, charging the fee on the side gives them more flexibility on how or what cost they want to pass on.

Are consumers stuck with having to pay these fees?

Probably.

As more and more companies find ways to pass on the fees, “we’re getting more comfortable paying them,” Marks said. “The airline industry introduced fees for baggage, has it gone away?”

In 2022, 23% of small businesses charged an extra fee to customers using credit cards, according to a survey of 530 small businesses last year by payments consultancy Strawhecker Group, which said more businesses would likely follow.

How to avoid credit card fees

You can always carry cash or look for a nearby ATM. But make sure that ATM transaction doesn’t carry fees too. If your credit card offers cash back, you may ultimately come out even or ahead, but you’ll have to wait to get that money back.

Credit card fees may end up like tipping, “most people just pay it and don’t think about it. But it adds up: a little and a little makes a lot,” Marks said.

Consumers also feel financial pain, why should they pay?

That’s what a handful of senators wonder, too. In June, a bipartisan group of senators, including Senate Majority Whip Dick Durbin (D-IL), and Senator Roger Marshall, M.D. (R-KS), proposed the Credit Card Competition Act of 2023 aimed at lowering the credit card processing fee for businesses and consumers. The bill was originally offered up in 2022 but didn’t advance in Congress.

Based on the argument that Visa and Mastercard have a duopoly on the credit card market (more than 80% of credit cards transactions are processed by them) and set the fee structure, the bill would ensure large credit card-issuing banks offer a choice of at least two networks over which an electronic credit transaction may be processed, senators said. By introducing more networks into every transaction, they believe the increased competition would lower fees for businesses and consumers.

“Our legislation would rein in the big banks and the credit card industry, drive down costs for convenience stores, gas stations, and other small businesses, and ultimately pass those savings down to consumers,” Senator Marshall said in a release.

Mastercard and Visa refute the notion that there’s no competition in the payments industry.

“There have never been more payment options for consumers and businesses,” Mastercard said in a statement in September. “In addition to cash and check, Mastercard aggressively competes with global and regional networks, buy now pay later providers, person-to-person and account-to-account services, real-time payments platforms (including from the Federal Reserve), digital currencies, wallet providers, and open banking companies.”

Government tries to curb fees: How much should credit card processing fees be? A new bill says not so high

Is legislation the answer to credit card fees?

Depends on whom you ask.

-

“Swipe fees that drive up costs for small merchants and prices for American families are already the highest in the industrialized world and are going nowhere but up,” said Doug Kantor, general counsel for the National Association of Convenience Stores. “Lack of competition is the problem, and the sooner the card industry can be made to compete, the better.”

-

Others blame the complicated fee structure. “There’s like 70 pages of rules on getting lower processing costs,” said Eric Cohen, chief executive of Merchant Advocate, which helps merchants navigate the complicated world of credit card processing fees to save them money.

-

EPC argues that credit card processing fees are necessary to pay for updated technology to secure payments, rewards and points and reduce credit for those who need it most, EPC said. Banks would tighten credit to lower-income populations or charge them higher fees to compensate for lost revenues, and merchants would simply choose the lowest price network to process cards instead of the safest.

“Consumers, workers, and small banks are going to be the biggest losers, because popular cash-back and rewards programs will disappear, fraud will likely explode, and millions of Americans could lose access to credit,” said EPC Chairman Richard Hunt.

Medora Lee is a money, markets, and personal finance reporter at USA TODAY. You can reach her at mjlee@usatoday.com and subscribe to our free Daily Money newsletter for personal finance tips and business news every Monday through Friday.

This article originally appeared on USA TODAY: Paying with credit card, not cash, increasingly costs you a fee upfront

Read the full article here

A Macy’s Employee Made Accounting Errors Worth $132 Million

Elon Musk Taught Himself to Code. Now It’s Your Turn.

5 Ways to Hire and Retain Top Talent in 2025

3 Simple Tips for Increasing Your Annual Recurring Revenue

Palantir assigned Street-high targets by Wedbush and BofA By Investing.com

How to Create a Unique Value Proposition (With Tips & Examples)

Are You Missing These Hidden Warning Signs When Hiring?

7 Common Things You Should Never Buy New

The DOJ Reportedly Wants Google to Sell Its Chrome Browser

This All-Access Pass to Learning Is Now $20 for Black Friday

Debt ceiling debate and its effect on the U.S. dollar

Debt ceiling default: Still no deal between parties

Stovall: If the U.S. defaults on its debt, all S&P 500 sectors will likely fall

What China's weaker-than-expected economy could mean for U.S. markets

A ‘Big Short’ investor sees financial disaster brewing in housing markets — again

-

Side Hustles6 days ago

Side Hustles6 days agoHow to Create a Unique Value Proposition (With Tips & Examples)

-

Investing5 days ago

Investing5 days agoAre You Missing These Hidden Warning Signs When Hiring?

-

Make Money5 days ago

Make Money5 days ago7 Common Things You Should Never Buy New

-

Side Hustles6 days ago

Side Hustles6 days agoThe DOJ Reportedly Wants Google to Sell Its Chrome Browser

-

Investing2 days ago

Investing2 days agoThis All-Access Pass to Learning Is Now $20 for Black Friday

-

Passive Income2 days ago

Passive Income2 days agoHow to Create a Routine That Balances Rest and Business Success

-

Investing5 days ago

Investing5 days agoGoogle faces call from DuckDuckGo for new EU probes into tech rule compliance By Reuters

-

Side Hustles3 days ago

Side Hustles3 days agoApple Prepares a New AI-Powered Siri to Compete With ChatGPT