Personal Finance

How to pay off $10,000 in credit card debt

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

When you make a financial plan, it might be challenging to figure out what to tackle first. Should you save for retirement, build an emergency savings account or pay off your debts? While all three of these financial goals are important, paying off credit card debt can jumpstart the rest of your financial goals by saving you money in fees and interest while boosting your credit score.

Even if you have thousands of dollars in credit card debt, you can pay it off sooner than you think with these five doable debt management strategies. Let’s take a look.

- Put yourself on a 1-year debt payoff plan

- Use a tried-and-true debt payoff strategy

- Consolidate the debt

- Seek help through debt relief

- Earn more with a new side hustle — or a new job

1. Put yourself on a 1-year debt payoff plan

A solid one-year debt payoff plan acknowledges how much money you need to come up with in small, achievable pockets to meet your goal.

Let’s imagine that your credit card carries a $10,000 balance, a 19.07% APR, and you make a payment of $300 every month. If you submit just the minimum payment each month, it will take you four years to pay off your balance, and you’ll pay more than $4,000 in interest!

But say you put yourself on a one-year payoff plan. Unfortunately, due to interest, you can’t just divide $10,000 by 12 and pay $833 a month — interest tacks on a pretty large amount. But you could pay off your credit card in a year if you paid roughly $950 a month for 12 months. Using a calculator will determine how much you’ll need to recompense each month to pay off your credit card in a year.

2. Use a tried-and-true debt payoff strategy

With a plan and goal in place, now it’s time to talk strategy. Some common techniques could be by paying more than your monthly credit card minimum, the debt snowball method, and the debt avalanche method.

Pay more than the minimum

As we just saw, interest rates can seriously add up. When you pay more than the minimum — even if you can’t afford to add hundreds of dollars to your usual dues — you can still shave significant interest.

This method is best if you need flexibility while still consistently chiseling away at your debt. As long as you put extra money — whatever you can realistically afford — toward your monthly credit card payment, you’ll shorten your repayment time and lower your total interest.

For example, say instead of the minimum $300 payment, you manage to add an extra $50 each month. Plugging that new number into a credit card payment calculator, you’ll see that even this small improvement will allow you to get out of credit card debt a year faster and save almost $1,500 in interest!

Debt snowball

If your $10,000 in credit card debt is spread across multiple cards and you need a positive incentive, this might be a good method for you. It can be great for when you really want to see progress quickly and have that win under your belt.

The snowball method is pretty straightforward: You put money towards the smallest debt you have. This allows you to see speedy results and can give you a boost of motivation — not unlike a snowball gaining momentum as it rolls down a hill. On the downside, reaching for the low-hanging fruit doesn’t save you as much on interest or cut your repayment time by as much because your larger debts will still be waiting for you on the other side.

Say you have $1,000 on one credit card and $9,000 on the other. Instead of focusing on the larger balance or splitting your extra payments between both, you’ll put all your extra money towards the $1,000 balance. Because the total is lower, you’re likely to pay it off much more quickly and can then move on to the $9,000 balance.

Debt avalanche

The debt avalanche method of repayment is also for those whose debt is spread across multiple accounts, but it aims to tackle truly crushing interest rates. This makes it a great option if you can’t seem to make any headway with your current strategy.

To use the debt avalanche method, organize your debts by interest rate and put all your extra cash towards the one with the highest interest rate. While it will likely take a while to see results, this method will save you more in interest and help you cut the amount of time it will take to pay off your total credit card balance. It can be tough to stick it out, though, so make sure you’re in it for the long haul and can patiently wait for the avalanche to gain steam!

As an example, take one card with an 18.00% APR and a second card with a 34.99% APR. You’ll want to feed all your extra money to the latter because its interest rate is nearly double the former.

3. Consolidate the debt

If you have more than one credit card with debt and would prefer a steady monthly payment, debt consolidation could be an option. Debt consolidation allows you to streamline your various credit card accounts — and their balances — into one account. There are two ways to consolidate credit card debt.

Debt consolidation loan

If you have a good credit score (generally 670-plus), a debt consolidation loan is probably a good choice for you. A good credit score means you’re more likely to qualify for low interest rates that will save you a lot of money compared to a credit card. But a debt consolidation loan is worth looking into even if your credit score isn’t stellar — especially if your credit card has a high interest rate.

To get a debt consolidation loan, you should apply for a personal loan with a bank, credit union, or online lender. Make sure you rate shop and compare interest rates, fees, loan terms (how many payments you’ll have to make until the loan is paid off), and monthly payment amounts.

Once you’re approved, the lender will deposit a lump sum into your bank account, which you’ll use to pay off your credit card. (Some lenders offer the ability to pay off your credit card balances directly.) After that, you’ll make your monthly payments to your personal loan rather than your credit card.

Consolidating your credit card debt with a loan can save you hundreds of dollars in interest and cut months or even years off your repayment time. It can even give your credit score a boost by diversifying the types of credit you have and lowering the percentage of your credit limit you’re currently using.

On the negative side, a hard credit inquiry (when applying for a debt consolidation loan) could ding your credit score in the short term.

Also, make sure you have a handle on your spending when taking on a loan. Not doing so could run up your credit card balance again, leaving you to pay off your personal loan and another high-interest balance on your credit card. Be careful to factor fees into your math when you take a look to see if personal loans are right for you.

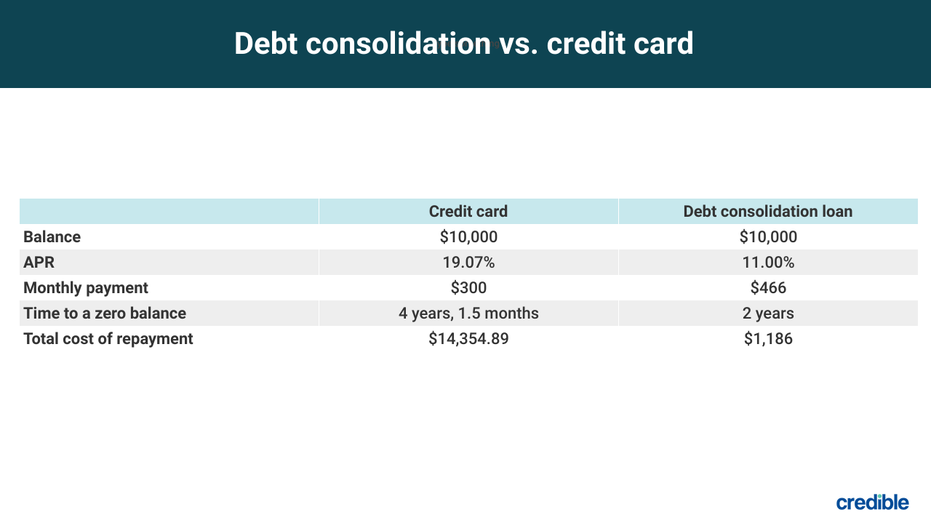

Say you take out a personal loan to pay off your credit card. Here’s an example of how much time and money you could save.

Even if you put that same monthly payment of $466 to your credit card in this scenario, you’ll pay about $2,326.79 in interest, and it’ll take three months longer to pay it off than it would with a loan. Use a personal loan calculator to see if a personal loan is a good choice for your situation.

0% APR credit card

Many credit cards offer a 0% promotional interest rate for balance transfer credit cards for a certain period — commonly, 12 to 21 months. This means you can use the balance transfer card to pay off another, and as long as you pay it off within the 0% introductory rate period, you’ll dodge paying interest.

A balance transfer credit card is a great option if you know for certain that you can zero the balance before the rate jumps up. Some cards also offer rewards, like points or cash back, that you can use to save money in other areas.

However, be aware of balance transfer credit card risks. Many cards charge a fee to do a balance transfer, so calculate that into your decision as to whether this is a good option for you. Also, you should be absolutely confident you can keep from running your credit card balance back up on the first card.

4. Seek help through debt relief

If other options don’t seem feasible for your financial situation — and credit card balance — you can still seek help with your hardship.

Debt settlement

If you’re really struggling to pay off credit card debt, you might want to consider this option. Basically, you’d be telling your credit card issuers that it’s better for them to take less than you owe as a sure thing rather than hoping you’ll be able to pay the balance off over time.

Credit card debt is unsecured, meaning the card issuer can’t take an asset, like your house, as a form of repayment. This gives you some negotiating leverage. By telling the credit card company that you’re struggling to make payments to the point of considering default or bankruptcy, they may be willing to negotiate to find a solution where they lose as little money as possible. (They might also offer hardship programs that temporarily pause or reduce your payments.)

Obviously, debt settlement can be a good solution for those who have a lump sum on hand to offer. But while this method can erase your credit card debt, it’s not a quick and easy solution. It could damage your credit for years, and there’s no guarantee your credit card company will agree to settle.

There are debt settlement companies you can hire to negotiate on your behalf, but they will likely charge fees and can’t guarantee success. Do your research to see if the increased effectiveness of having professionals negotiate on your behalf is worth the bill.

Debt management program

Professional debt management is another option to consider if you’re in dire straits. Unlike the companies mentioned above, there are nonprofit resources like the National Foundation for Credit Counseling (NFCC) that can help you with a plan.

This method means working with an organization like an NFCC-approved agency to get on a repayment schedule that works for you and your credit card company. Credit card companies may lower or waive your interest rates and fees, reducing the total amount owed. Once you’ve reached an agreement, you’ll make your monthly payment to the NFCC who will pass it on to the credit card company, ensuring you stick to the plan.

This is a great option if you’re truly unable to manage your credit card debt and are looking for professional help to make better financial choices. After a term of three to five years, you’ll have repaid your debts. That said, this method could ding your credit score, close off your access to new credit for some time, and might not reduce your actual balance. You can reach out to an NFCC-approved agency’s counselor to discuss your options and see if this method is right for your situation.

Bankruptcy

Off all the options listed here, bankruptcy comes with the biggest downside and should only be entered into as a last resort. If your only outstanding balance is $10,000 in credit card debt, bankruptcy is almost certainly not the right choice for you. However, if $10,000 in credit card debt is just the tip of the iceberg, you can discuss your options with a bankruptcy attorney.

If you’re looking at bankruptcy as a solution to credit card debt, you’re likely looking at Chapter 13 bankruptcy. This bankruptcy plan allows you to work with your credit card company and a judge to establish a three-year repayment plan.

While this will allow you to emerge in three years with no debts, the consequences of bankruptcy are severe. First of all, you’ll have to pay to file for bankruptcy and for an attorney to represent you, which can cost thousands of dollars. Though you could represent yourself, it’s best to have a qualified expert to deal with complex legal issues that can arise.

Also, even after you’ve paid off your three-year plan, bankruptcy will impact you for years to come. Your credit score will plummet and bankruptcy will stay on your credit report for up 7 to 10 years. Make sure you’ve exhausted all of your options and consult with experts before filing for bankruptcy.

5. Earn more with a new side hustle — or a new job

Though easier said than done, bringing in more money is an excellent way to pay off your credit card balance faster.

While a better-paying job is a great option that could require time for training, upskilling or career transitioning, a side hustle is good for those who have extra time — and a lot of options open up if you have a car or spare room. Some gig economy companies, like Uber, GrubHub, Instacart and Airbnb have a relatively streamlined sign-up process available online or through their app. You could also sell clothes on apps like Poshmark, pick up a part-time job at a grocery store or other retailer, or find freelance work in your field.

The great thing about side hustles is that you can immediately put your earned money toward your credit card debt, while keeping your current budget the same. And if you can find freelance work in your field, you can gain job experience, connections and extra income simultaneously. However, if you are short on free time due to family or other present obligations, it might not be your best option.

Of course, there’s also the case of taxes and maintenance costs to factor in when you’re calculating how much you’ll make from a side hustle.

On the other hand, seeking out career opportunities is a great idea whether or not you have credit card debt. Seek out positions with a higher salary and/or remote privileges so that you can put more earnings or your commute’s costs toward your credit card balance.

Read the full article here