Personal Finance

Today’s lowest mortgage rates? Shorter terms remain below 6% | June 14, 2023

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

Based on data compiled by Credible, mortgage rates for home purchases have remained stable for two key terms, risen for another, and fell for one more since yesterday.

Rates last updated on June 14, 2023. These rates are based on the assumptions shown here. Actual rates may vary. Credible, a personal finance marketplace, has 5,000 Trustpilot reviews with an average star rating of 4.7 (out of a possible 5.0).

What this means: Mortgage rates for both 10- and 30-year terms have held steady since yesterday, remaining at 5.625% and 6.375%, respectively. Meanwhile, rates for 20-year terms have edged up to 6.375%. Additionally, rates for 15-year terms have dropped to 5.75%. Borrowers looking for a lower monthly payment should consider either of today’s longer terms at 6.375%. Homebuyers who would rather save the most on interest should instead consider today’s lowest rate, 10-year terms at 5.625%.

To find great mortgage rates, start by using Credible’s secured website, which can show you current mortgage rates from multiple lenders without affecting your credit score. You can also use Credible’s mortgage calculator to estimate your monthly mortgage payments.

Based on data compiled by Credible, mortgage refinance rates have risen for one key term, held steady for one, and fell for two others since yesterday.

Rates last updated on June 14, 2023. These rates are based on the assumptions shown here. Actual rates may vary. With 5,000 reviews, Credible maintains an “excellent” Trustpilot score.

What this means: Mortgage refinance rates have remained stable for 20-year terms at 6.375%. Meanwhile, rates for 15- and 30-year terms have fallen to 5.625% and 6.25%, respectively. Additionally, rates for 10-year terms have jumped up by a quarter of a percentage point to 5.875%. Homeowners who would like to maximize their interest savings should consider today’s lowest rate, 15-year terms at 5.625%. Borrowers who would rather have a smaller monthly payment should instead consider 30-year terms at 6.25%.

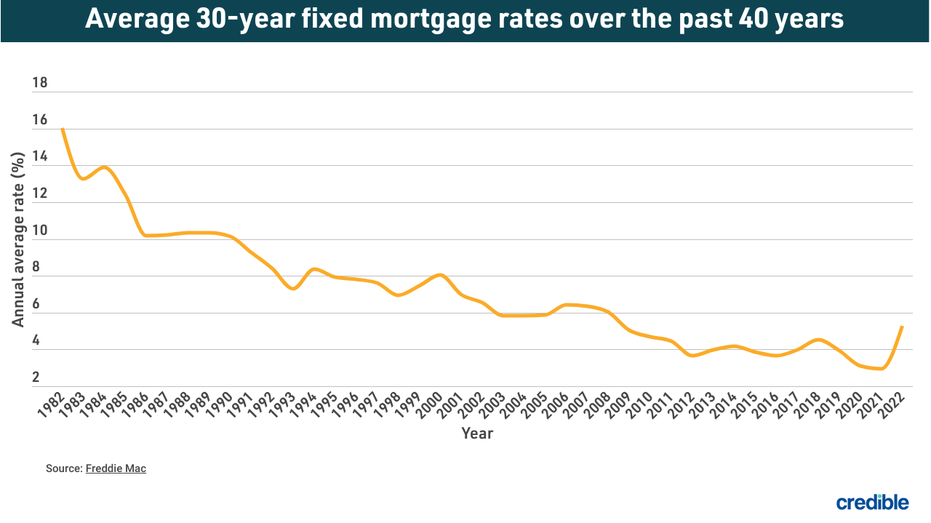

How mortgage rates have changed over time

Today’s mortgage interest rates are well below the highest annual average rate recorded by Freddie Mac — 16.63% in 1981. A year before the COVID-19 pandemic upended economies across the world, the average interest rate for a 30-year fixed-rate mortgage for 2019 was 3.94%. The average rate for 2021 was 2.96%, the lowest annual average in 30 years.

The historic drop in interest rates means homeowners who have mortgages from 2019 and older could potentially realize significant interest savings by refinancing with one of today’s lower interest rates. When considering a mortgage or refinance, it’s important to take into account closing costs such as appraisal, application, origination and attorney’s fees. These factors, in addition to the interest rate and loan amount, all contribute to the cost of a mortgage.

How Credible mortgage rates are calculated

Changing economic conditions, central bank policy decisions, investor sentiment and other factors influence the movement of mortgage rates. Credible average mortgage rates and mortgage refinance rates reported in this article are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 700 credit score and is borrowing a conventional loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage rates reported here will only give you an idea of current average rates. The rate you actually receive can vary based on a number of factors.

Getting a mortgage vs. renting

If you’re wondering if you should buy a house or continue renting, no single answer is right for everyone. Whether you should buy or continue renting depends on many factors, including your personal financial situation, long-term goals, preferred lifestyle and market conditions in your area.

Buying a home does come with some distinct advantages that you can’t get from renting, including …

- You can build equity. Home equity can help you build long-term wealth.

- You can personalize your living space more than with a rental that someone else owns.

- Owning a home can provide intangible benefits like pride of ownership, a sense of community and stability.

- Your mortgage payment may be less than rents in your area.

- Mortgage interest is usually tax-deductible.

If you’re trying to find the right mortgage rate, consider using Credible. You can use Credible’s free online tool to easily compare multiple lenders and see prequalified rates in just a few minutes.

Have a finance-related question, but don’t know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.

Read the full article here

Looking to Sell Your Company? Here’s a Potentially Lucrative Exit Plan Every Business Needs to Consider.

How to Make Focus an Unbreakable Habit in 2025: The Secret Weapon for Superhuman Focus

5 Benefits of ‘Ick’ Franchise Industries

Join the Highest-Growing Industry in 2025 With This $60 Cybersecurity E-Learning Bundle

Morgan Stanley boosts consumer finance outlook for 2025 By Investing.com

KFC Announces Saucy, a Chicken Tenders-Focused Spinoff

Palantir, Anduril join forces with tech groups to bid for Pentagon contracts, FT reports By Reuters

4 Ways Content Can Make or Break the Customer Experience

Why Emotional Intelligence Is the Key to High-Impact Leadership

How to Build a Legacy of Leadership in Your Business in Six Proven Strategies

Debt ceiling debate and its effect on the U.S. dollar

Debt ceiling default: Still no deal between parties

Stovall: If the U.S. defaults on its debt, all S&P 500 sectors will likely fall

What China's weaker-than-expected economy could mean for U.S. markets

A ‘Big Short’ investor sees financial disaster brewing in housing markets — again

-

Side Hustles7 days ago

Side Hustles7 days agoKFC Announces Saucy, a Chicken Tenders-Focused Spinoff

-

Investing7 days ago

Investing7 days agoPalantir, Anduril join forces with tech groups to bid for Pentagon contracts, FT reports By Reuters

-

Side Hustles6 days ago

Side Hustles6 days ago4 Ways Content Can Make or Break the Customer Experience

-

Passive Income4 days ago

Passive Income4 days agoWhy Emotional Intelligence Is the Key to High-Impact Leadership

-

Side Hustles6 days ago

Side Hustles6 days agoHow to Build a Legacy of Leadership in Your Business in Six Proven Strategies

-

Personal Finance3 days ago

Personal Finance3 days agoTop personal finance New Year's resolutions for 2025

-

Side Hustles7 days ago

Side Hustles7 days agoHow Mentorship Shapes Resilient Leaders and Thriving Teams

-

Passive Income7 days ago

Passive Income7 days agoThe Last Pen You’ll Ever Have to Buy — Never Run Out of Ink Again With the ForeverPen