Personal Finance

Can you get a home equity loan with bad credit — and should you?

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

Having a bad credit score can make it harder to get approved for a loan. Fortunately, you can still qualify for a home equity loan, even if your credit is less than ideal. By taking out a home equity loan, you might even be able to improve your credit score by making consistent, on-time loan payments.

But just because you might be able to get a home equity loan doesn’t always mean you should. It’s important to consider the benefits and drawbacks of taking out such a loan before you apply. This will help you make sure it’s the right decision for your unique financial situation.

Credible doesn’t offer home equity loans, but you can compare prequalified mortgage refinance rates from multiple lenders in just a few minutes.

What is a home equity loan?

A home equity loan is a second mortgage that lets you borrow against the equity in your home. Equity is the difference between your mortgage balance and the current value of your home. If you qualify, you’ll receive a lump sum of money that you can use for nearly anything, including debt consolidation, medical expenses and paying for big-ticket items.

Like personal loans, home equity loans are installment loans. This means you must make fixed monthly payments over a set period of time until you pay back what you borrowed.

Your monthly payments will typically include the principal balance plus any interest and lender’s fees (like origination fees for processing the loan application). If you consistently make on-time payments, you’ll be able to pay off the entire loan by the end of the repayment term.

Home equity loans can be a great tool if you know how to use them. For example, you could use one to renovate your home — instead of a home improvement loan — to further increase the value of your property. Or you could consolidate high-interest debts into a loan with a lower interest rate.

This type of financing might be easier to get than other loans — like unsecured personal loans — if you have bad credit. They may also have lower interest rates because the loan is secured with your home as collateral.

But these loans aren’t for everyone. Your borrowing amount and interest rate both depend on your credit score, income and debt-to-income (DTI) ratio. To qualify, you’ll also need to have enough equity in your home. Most mortgage lenders will limit your borrowing amount to a maximum of 80% of your home equity.

Additionally, because home equity loans are secured with your property, the lender could foreclose on your home if you fail to make payments.

Understand your credit health

Your credit score plays a vital role in determining if you’ll qualify for any type of financing, whether it’s a home equity loan or home equity line of credit (HELOC). Minimum credit score requirements will vary among lenders. But you’ll likely need good to excellent credit to qualify for a home equity loan.

Typically, a credit score of 670 to 739 is considered “good credit.” The better your score, the higher your approval odds for loans, lines of credit and other forms of financing. Additionally, if you have a higher credit score, you’re more likely to qualify for lower rates and better terms.

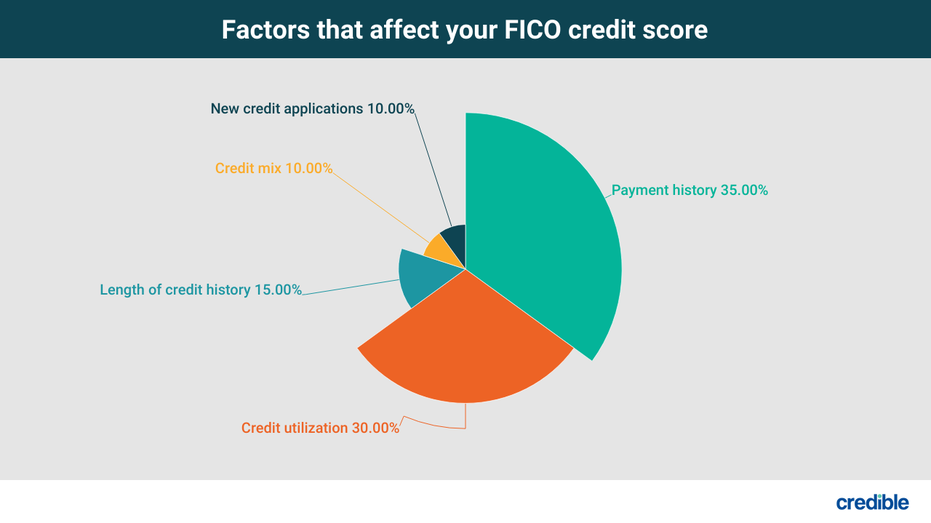

Here are several factors that make up your credit score:

Other factors like recent bankruptcies, foreclosures and errors on your credit report can also negatively impact your credit score.

If you’re not sure where your credit stands, you can request a free copy of your credit report online. Review it carefully for any areas that need work. Check for errors, such as incorrect late payments or charge-offs, and dispute them with the appropriate credit bureau to potentially boost your score.

If your credit needs some work, here are a few ways to boost your score:

- Make payments on time. Even one missed payment can drag down your credit score, so getting all of your monthly payments in on time will help you build credit.

- Pay down existing debt. Paying off debt, like credit card balances or other loans, can help reduce your credit utilization ratio. Your credit utilization is how much of your revolving credit youâre using divided by your credit limit. Having a low credit utilization ratio shows lenders that you can responsibly manage your debts.

- Keep older accounts active. This adds to the average age of your credit. Since credit history makes up 15% of your credit score, a longer credit history is good for your score.

- Diversify your credit. Having a diverse credit mix also helps you build credit. If, for example, you only have a credit card, applying for a small personal loan can improve this aspect of your credit profile.

What about debt-to-income ratio?

Debt-to-income (DTI) ratio is another important factor that lenders consider when deciding whether to approve your loan application. Your DTI ratio is how much of your monthly income goes toward paying off existing debt, expressed as a percentage.

To determine your DTI ratio, add up all of your monthly debt payments, including student loans, credit cards, mortgage or rent, or child support. Then, divide that amount by your gross monthly income.

For example, say you make $4,500 a month and spend $2,500 on debt payments. Your DTI ratio would be 56%.

Although your DTI ratio doesn’t directly affect your credit score, you might not qualify for financing if yours is too high. To qualify for a home equity loan, aim to keep your DTI no higher than 43%.

Types of home equity loans for bad credit

If you have poor or fair credit, here are several types of home equity loans to consider:

- FHA cash-out refinancing: The Federal Housing Administration (FHA) doesnât offer home equity loans, but it does offer cash-out refinancing. This lets you refinance your home into a larger home loan. Youâll get the difference in a lump sum that you can use as you see fit.

- Subprime home equity loans: These loans typically have less stringent lending requirements than traditional loans, making them more ideal for bad credit borrowers. However, they may also come with higher interest rates or less ideal repayment terms. These loans are secured with the equity in your home as collateral.

- Personal loans for bad credit: Some banks, credit unions and online lenders offer personal loans for borrowers with poor credit. When you have a low credit score, lenders may be concerned that youâll default on payments. To offset that risk, bad credit personal loans often come with higher interest rates or shorter repayment terms. You may be able to get a lower interest rate by offering collateral, like your home or car.

- Home equity lines of credit: A HELOC is a type of revolving credit that you can borrow from as needed over a set amount of time known as the “draw period.” During this time, youâll only need to make interest payments on the amount you borrow. Once the draw period ends, youâll enter the repayment period and make regular payments until you pay off the full amount.HELOCs are flexible, but typically come with variable interest rates, meaning your payments may fluctuate over time. This type of financing is also secured by your home, so you risk for closure if you fall behind on payments.

WHERE TO FIND HOME LOANS FOR BAD CREDIT

Pros of getting a home equity loan with bad credit

Taking out a home equity loan with bad credit or limited credit history comes with several benefits, including:

- Flexible loan use: You can use the money from a home equity loan for nearly any reason, including debt consolidation, home repairs, medical bills, weddings or paying for college.

- Lenient eligibility requirements: Since these are secured loans, youâll likely be able to qualify even if you donât have good credit.

- Lower interest rates: Home equity loans usually come with lower interest rates than personal loans and other home improvement loans because theyâre secured with your home as collateral.

- Fixed repayment terms and rates: Home equity loans are fixed-rate installment loans, meaning your payments wonât fluctuate and youâll have a set timeline to repay your loan, usually over five to 15 years.

Cons of getting a home equity loan with bad credit

Before applying for a home equity loan, here are some downsides to consider:

- Risk of losing your home: Since the loan is secured with your home equity, you could lose your property if you default on payments.

- Closing costs and other fees: As a second mortgage loan, home equity loans sometimes come with additional fees like closing costs or appraisal fees. Closing costs for home loans typically range from 2% to 5% of your loan amount, while appraisal fees can cost as much as $500.

- Potentially lower loan amounts: Your borrowing amount depends on how much equity you have in your home and your credit score. If you have poor credit, you might qualify for a smaller amount.

- Must have significant home equity: If you donât have enough home equity, you may not qualify for a loan at all. Home equity loan lenders typically require that you have 80% equity in your home.

- Risk of spending more than necessary: Itâs easy to take out a larger loan than you actually need. When applying for any type of financing, be sure to only borrow what you can afford to comfortably repay.

Why it might be worth improving your credit before borrowing

Although you may qualify for a home equity loan with bad credit, it might be better to improve your credit score before applying for one. This is because your credit score plays a major role in determining if you can get a loan.

Review your credit report for errors, make on-time payments on all of your bills, and lower your credit utilization to boost your credit score. By improving your credit, you can increase your approval odds and qualify for better rates and terms.

If you decide a refinance is a better fit for your financial goals, you can compare mortgage refinance rates from multiple lenders in minutes using Credible.

Read the full article here

5 Financial Blind Spots That Could Be Preventing You From Making More Money

Boost Business Efficiency with Five Years of Control D for $40

What to Expect as 7-Eleven U.S. Makes Japanese-Inspired Changes

5 Secrets to Successfully Launch Your First Paid Product

Today's mortgage rates remain unchanged for 15- and 30-year terms | July 26, 2024

Gas prices drop as demand for driving fizzles out: AAA

Crowdstrike CEO Responds to Causing Largest IT Outage in History

How to Build A Startup, From an Early Lyft, Twitch Investor

The Top 5 AI Tools That Can Revolutionize Your Workflow and Boost Productivity

NLRB Drops Expanded Joint Employer Appeal

Debt ceiling debate and its effect on the U.S. dollar

Debt ceiling default: Still no deal between parties

Stovall: If the U.S. defaults on its debt, all S&P 500 sectors will likely fall

What China's weaker-than-expected economy could mean for U.S. markets

A ‘Big Short’ investor sees financial disaster brewing in housing markets — again

-

Personal Finance7 days ago

Personal Finance7 days agoGas prices drop as demand for driving fizzles out: AAA

-

Investing7 days ago

Investing7 days agoCrowdstrike CEO Responds to Causing Largest IT Outage in History

-

Side Hustles7 days ago

Side Hustles7 days agoHow to Build A Startup, From an Early Lyft, Twitch Investor

-

Passive Income7 days ago

Passive Income7 days agoThe Top 5 AI Tools That Can Revolutionize Your Workflow and Boost Productivity

-

Passive Income5 days ago

Passive Income5 days agoNLRB Drops Expanded Joint Employer Appeal

-

Side Hustles7 days ago

Side Hustles7 days agoJake Paul: Mindset Hacks, Mike Tyson Fight, Embracing Fear

-

Investing7 days ago

Investing7 days agoBoeing to supply E-7 in first major win since plea deal By Reuters

-

Side Hustles6 days ago

Side Hustles6 days ago10 Effective Growth Marketing Strategies for Your Startup