Debt Management

How to Find Out if Refinancing is Right For Your Student Loans

The average student loan debt in 2017 is $37,172. This kind of debt is not something that many people can pay off quickly. Instead, they make monthly payments and pay it down over the course of multiple years. Depending on the financial situation, these payments may not be an issue.

In other cases, the burden is too much, or the interest is too high. In these cases, refinancing the loan could be a solution to the issue. This doesn’t take the loan away, but it does offer more ways to control it. Let’s find out how you can decide if this is the right approach for you in your financial journey.

Analyzing The Pros and Cons of Refinancing Student Loans

Given the current costs of tuition, it’s not uncommon for students to take out loans to fund their college education. In many cases, these students don’t need to start paying on their loans until after they’ve graduated.

This is great for convenience, but once they have their degree, the monthly bills start rolling in. Constrained budgets and searching for jobs can take a toll on the new graduates. Student loans add further stress to this equation.

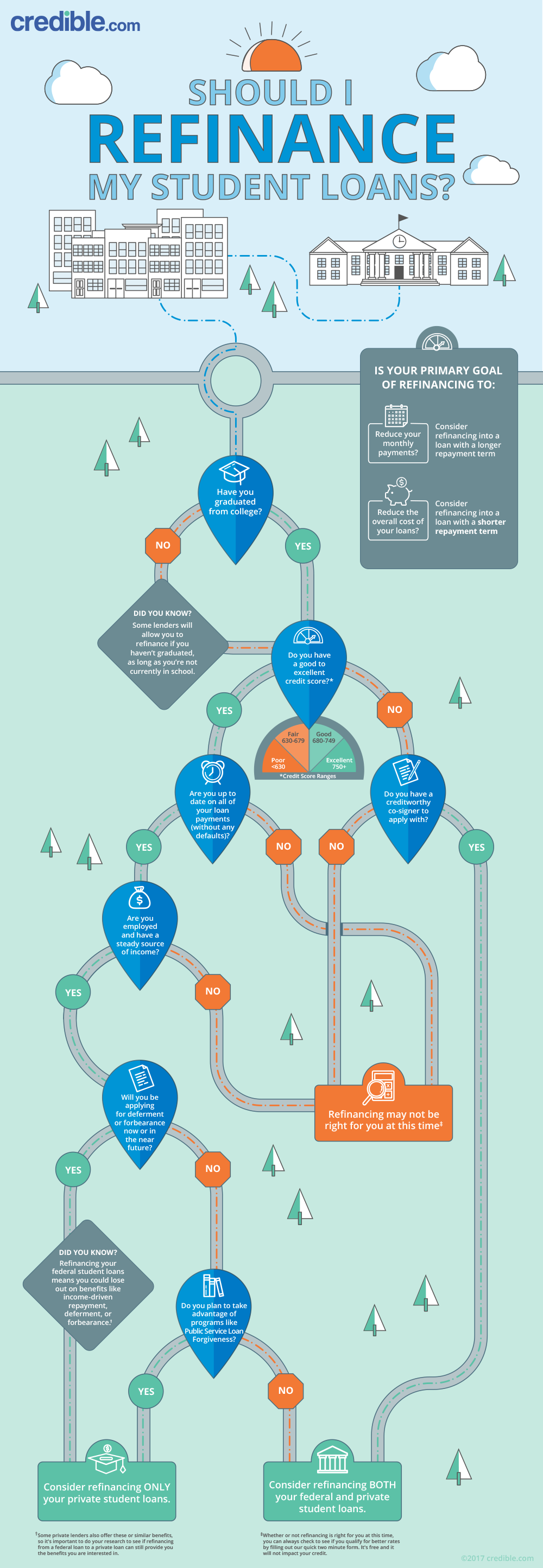

For many people with student loans, refinancing offers a solution that significantly change their situation and give them more control over their student loans. As you set out to explore your options for refinancing with private lenders, you’ll begin to see many of the benefits that refinancing offers:

- A choice between Fixed and Variable Interest rates: If you want to lock in a new interest rate, you have that option. Variable interest rates offer more flexible options, but do have the potential to go up rather than down. If you plan to pay down the loan quickly, variable interest rates do tend to start lower.

- A single monthly payment: If you have multiple loans, refinancing can consolidate them into one loan through a private lender. This will allow you to make one payment each month towards your entire student debt.

- Flexible Terms: During the refinancing process, you can choose to change the terms of the loan. This will allow for a lower interest rate or a different repayment term. If you wish to have lower monthly payments, you can make the loan term longer as needed.

There are some downsides to refinancing. If you have federal loans, you will lose out on benefits offered by them such as loan forgiveness or income-based repayment plans. Your current credit score will also influence the options you have while refinancing. If you’ve struggled with making payments, a lower credit score may affect your options.

The infographic below from Credible.com illustrates the thought processes and decisions people often make when they are considering a refinancing option.

Read the full article here

5 Financial Blind Spots That Could Be Preventing You From Making More Money

Boost Business Efficiency with Five Years of Control D for $40

What to Expect as 7-Eleven U.S. Makes Japanese-Inspired Changes

5 Secrets to Successfully Launch Your First Paid Product

Today's mortgage rates remain unchanged for 15- and 30-year terms | July 26, 2024

Gas prices drop as demand for driving fizzles out: AAA

Crowdstrike CEO Responds to Causing Largest IT Outage in History

How to Build A Startup, From an Early Lyft, Twitch Investor

The Top 5 AI Tools That Can Revolutionize Your Workflow and Boost Productivity

NLRB Drops Expanded Joint Employer Appeal

Debt ceiling debate and its effect on the U.S. dollar

Debt ceiling default: Still no deal between parties

Stovall: If the U.S. defaults on its debt, all S&P 500 sectors will likely fall

What China's weaker-than-expected economy could mean for U.S. markets

A ‘Big Short’ investor sees financial disaster brewing in housing markets — again

-

Personal Finance7 days ago

Personal Finance7 days agoGas prices drop as demand for driving fizzles out: AAA

-

Investing7 days ago

Investing7 days agoCrowdstrike CEO Responds to Causing Largest IT Outage in History

-

Side Hustles6 days ago

Side Hustles6 days agoHow to Build A Startup, From an Early Lyft, Twitch Investor

-

Passive Income7 days ago

Passive Income7 days agoThe Top 5 AI Tools That Can Revolutionize Your Workflow and Boost Productivity

-

Passive Income5 days ago

Passive Income5 days agoNLRB Drops Expanded Joint Employer Appeal

-

Side Hustles6 days ago

Side Hustles6 days agoJake Paul: Mindset Hacks, Mike Tyson Fight, Embracing Fear

-

Investing7 days ago

Investing7 days agoBoeing to supply E-7 in first major win since plea deal By Reuters

-

Side Hustles5 days ago

Side Hustles5 days ago10 Effective Growth Marketing Strategies for Your Startup